Page 306 - Full Book_24.4.2021

P. 306

NOTES TO THE

FINANCIAL STATEMENTS

for the financial year ended 31 december 2020 (continUed)

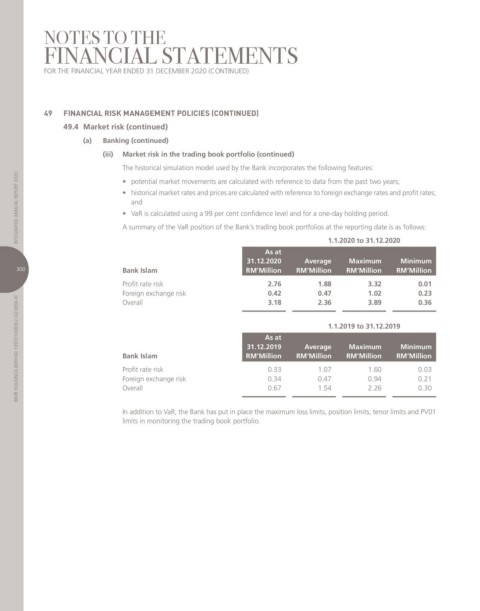

49 FINANCIAL RISk MANAGEMENT POLICIES (CONTINUED)

49.4 Market risk (continued)

(a) Banking (continued)

(iii) Market risk in the trading book portfolio (continued)

the historical simulation model used by the bank incorporates the following features:

inteGrated annUal rePort 2020 • historical market rates and prices are calculated with reference to foreign exchange rates and profit rates;

• potential market movements are calculated with reference to data from the past two years;

and

• VaR is calculated using a 99 per cent confidence level and for a one-day holding period.

a summary of the var position of the bank’s trading book portfolios at the reporting date is as follows:

As at 1.1.2020 to 31.12.2020

31.12.2020 Average Maximum Minimum

300 Bank Islam RM’Million RM’Million RM’Million RM’Million

Profit rate risk 2.76 1.88 3.32 0.01

foreign exchange risk 0.42 0.47 1.02 0.23

bimb holdinGS berhad 199701008362 (423858-X) Bank Islam RM’Million RM’Million RM’Million RM’Million

0.36

2.36

3.89

3.18

overall

1.1.2019 to 31.12.2019

As at

Average

Minimum

Maximum

31.12.2019

1.07

0.03

1.60

Profit rate risk

0.33

0.94

0.21

foreign exchange risk

0.34

0.47

2.26

0.30

overall

1.54

0.67

in addition to var, the bank has put in place the maximum loss limits, position limits, tenor limits and Pv01

limits in monitoring the trading book portfolio.