Page 305 - Full Book_24.4.2021

P. 305

NOTES TO THE

FINANCIAL STATEMENTS in retrospect

|

for the financial year ended 31 december 2020 (continUed)

the Will to Suceed

|

49 FINANCIAL RISk MANAGEMENT POLICIES (CONTINUED)

49.4 Market risk (continued)

(a) Banking (continued) achieving a leading repute

(ii) profit rate risk in the banking book portfolio

Profit rate risk in the banking book portfolio is managed and controlled using measurement tool known as |

earnings-at-risk (“ear”) and economic value of equity (“eve”).

the bank monitors the sensitivity of ear and eve under varying profit rate scenarios (i.e. simulation

modeling). the model is a combination of standard and non-standard scenarios relevant to the local market.

the standard scenarios include the parallel fall or rise in the profit rate curve and historical simulation. these Paving the Way for a Sustainable future

scenarios assume no management action. hence, it does not incorporate actions that would be taken by

the bank’s treasury to mitigate the impact of the profit rate risk. in reality, depending on the view on future

market movements, the bank’s treasury would proactively manage and strategize to change the profit rate

exposure profile to minimise losses and to optimise net revenues. the bank’s hedging and risk mitigation

strategies range from the use of derivative financial instruments, such as profit rate swaps, to more intricate

hedging strategies to address inordinate profit rate risk exposures.

299

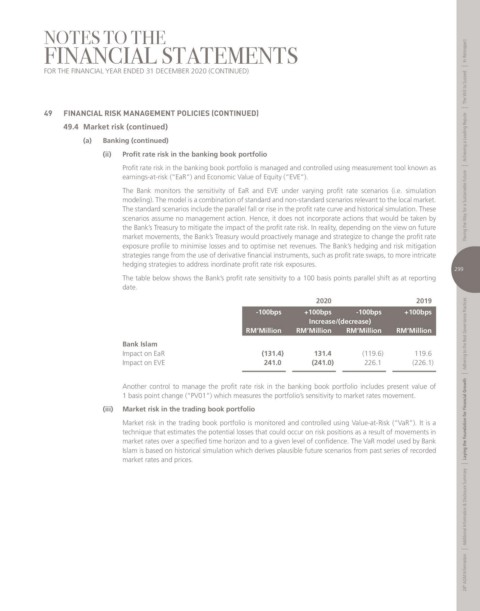

the table below shows the bank’s profit rate sensitivity to a 100 basis points parallel shift as at reporting

date.

2020 2019

-100bps +100bps -100bps +100bps

Increase/(decrease)

RM’Million RM’Million RM’Million RM’Million adhering to the best Governance Practices

Bank Islam

impact on ear (131.4) 131.4 (119.6) 119.6

impact on eve 241.0 (241.0) 226.1 (226.1)

|

another control to manage the profit rate risk in the banking book portfolio includes present value of

1 basis point change (“Pv01”) which measures the portfolio’s sensitivity to market rates movement.

(iii) Market risk in the trading book portfolio

market risk in the trading book portfolio is monitored and controlled using value-at-risk (“var”). it is a Laying the Foundation for Financial Growth

technique that estimates the potential losses that could occur on risk positions as a result of movements in

market rates over a specified time horizon and to a given level of confidence. the var model used by bank

islam is based on historical simulation which derives plausible future scenarios from past series of recorded

market rates and prices.

|

additional information & disclosure Summary

|

24 th aGm information