Page 325 - Full Book_24.4.2021

P. 325

NOTES TO THE

FINANCIAL STATEMENTS in retrospect

|

for the financial year ended 31 december 2020 (continUed)

the Will to Suceed

|

50 TAkAFUL RISk MANAGEMENT (CONTINUED)

(a) Family Takaful Fund (continued)

Key assumptions achieving a leading repute

reserves for all plans were valued on a basis that the appointed actuary considers adequate and appropriate,

and in-line with the valuation basis set out by bnm in respect of the Guidelines on valuation basis for liabilities of family |

takaful business (bnm/rh/Gl 004-20) and risk-based capital framework for takaful operator.

the key assumptions to which the estimation of actuarial liabilities is particularly sensitive to the followings:

– Mortality and morbidity rates Paving the Way for a Sustainable future

this is significant for contracts with significant coverage for death, total permanent disability and critical illness and

the increase in the mortality or morbidity rates would have direct impact on the liability.

– Discount rate

as the liabilities represents the present value of future cash outflow, a reduction in discount rate would have an

increasing impact on the liabilities and vice-versa.

– Surrender rate 319

this is only applicable to long-term products, where when the rate is reduced (products with Pif) or increased

(products without Pif), the impact is an increase of the liability.

Sensitivities

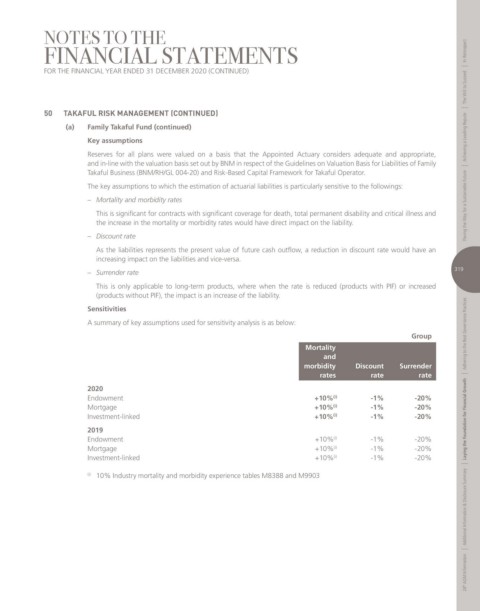

a summary of key assumptions used for sensitivity analysis is as below:

Group adhering to the best Governance Practices

Mortality

and

morbidity Discount Surrender

rates rate rate |

2020

endowment +10% (i) -1% -20%

mortgage +10% (i) -1% -20%

investment-linked +10% (i) -1% -20% Laying the Foundation for Financial Growth

2019

(i)

Endowment +10% -1% -20%

Mortgage +10% -1% -20%

(i)

Investment-linked +10% -1% -20%

(i)

|

additional information & disclosure Summary

(i) 10% Industry mortality and morbidity experience tables M8388 and M9903

|

24 th aGm information