Page 238 - Full Book_24.4.2021

P. 238

NOTES TO THE

FINANCIAL STATEMENTS

for the financial year ended 31 december 2020 (continUed)

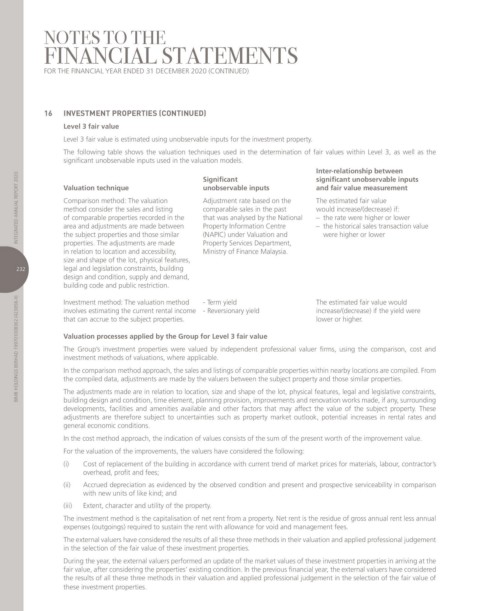

16 INVESTMENT PROPERTIES (CONTINUED)

Level 3 fair value

level 3 fair value is estimated using unobservable inputs for the investment property.

the following table shows the valuation techniques used in the determination of fair values within level 3, as well as the

significant unobservable inputs used in the valuation models.

Valuation technique Significant Inter-relationship between

inteGrated annUal rePort 2020 comparison method: the valuation adjustment rate based on the the estimated fair value

significant unobservable inputs

unobservable inputs

and fair value measurement

would increase/(decrease) if:

comparable sales in the past

method consider the sales and listing

that was analysed by the national

of comparable properties recorded in the

– the rate were higher or lower

– the historical sales transaction value

Property information centre

area and adjustments are made between

the subject properties and those similar

properties. the adjustments are made

Property Services department,

in relation to location and accessibility, (naPic) under valuation and were higher or lower

ministry of finance malaysia.

size and shape of the lot, physical features,

232 legal and legislation constraints, building

design and condition, supply and demand,

building code and public restriction. - term yield the estimated fair value would

bimb holdinGS berhad 199701008362 (423858-X) that can accrue to the subject properties. lower or higher.

investment method: the valuation method

involves estimating the current rental income - reversionary yield

increase/(decrease) if the yield were

Valuation processes applied by the Group for Level 3 fair value

the Group’s investment properties were valued by independent professional valuer firms, using the comparison, cost and

investment methods of valuations, where applicable.

in the comparison method approach, the sales and listings of comparable properties within nearby locations are compiled. from

the compiled data, adjustments are made by the valuers between the subject property and those similar properties.

the adjustments made are in relation to location, size and shape of the lot, physical features, legal and legislative constraints,

building design and condition, time element, planning provision, improvements and renovation works made, if any, surrounding

developments, facilities and amenities available and other factors that may affect the value of the subject property. these

adjustments are therefore subject to uncertainties such as property market outlook, potential increases in rental rates and

general economic conditions.

in the cost method approach, the indication of values consists of the sum of the present worth of the improvement value.

for the valuation of the improvements, the valuers have considered the following:

(i) cost of replacement of the building in accordance with current trend of market prices for materials, labour, contractor’s

overhead, profit and fees;

(ii) accrued depreciation as evidenced by the observed condition and present and prospective serviceability in comparison

with new units of like kind; and

(iii) extent, character and utility of the property.

the investment method is the capitalisation of net rent from a property. net rent is the residue of gross annual rent less annual

expenses (outgoings) required to sustain the rent with allowance for void and management fees.

the external valuers have considered the results of all these three methods in their valuation and applied professional judgement

in the selection of the fair value of these investment properties.

during the year, the external valuers performed an update of the market values of these investment properties in arriving at the

fair value, after considering the properties’ existing condition. in the previous financial year, the external valuers have considered

the results of all these three methods in their valuation and applied professional judgement in the selection of the fair value of

these investment properties.