Page 295 - Full Book_24.4.2021

P. 295

NOTES TO THE

FINANCIAL STATEMENTS in retrospect

|

for the financial year ended 31 december 2020 (continUed)

the Will to Suceed

|

49 FINANCIAL RISk MANAGEMENT POLICIES (CONTINUED)

49.3 Credit risk (continued)

Banking (continued) achieving a leading repute

(iii) Credit quality of financing, advances and others (continued)

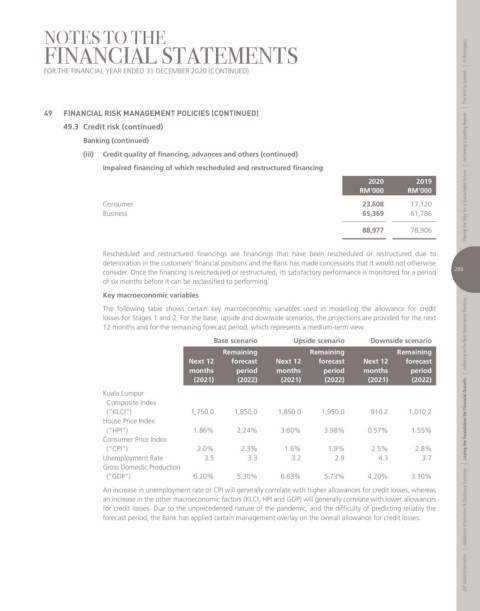

Impaired financing of which rescheduled and restructured financing |

2020 2019

RM’000 RM’000

consumer 23,608 17,120 Paving the Way for a Sustainable future

business 65,369 61,786

88,977 78,906

rescheduled and restructured financings are financings that have been rescheduled or restructured due to

deterioration in the customers’ financial positions and the bank has made concessions that it would not otherwise

consider. once the financing is rescheduled or restructured, its satisfactory performance is monitored for a period 289

of six months before it can be reclassified to performing.

Key macroeconomic variables

the following table shows certain key macroeconomic variables used in modelling the allowance for credit

losses for Stages 1 and 2. for the base, upside and downside scenarios, the projections are provided for the next

12 months and for the remaining forecast period, which represents a medium-term view.

Base scenario Upside scenario Downside scenario adhering to the best Governance Practices

Remaining Remaining Remaining

Next 12 forecast Next 12 forecast Next 12 forecast

months period months period months period

|

(2021) (2022) (2021) (2022) (2021) (2022)

Kuala lumpur

composite index

(“Klci”) 1,750.0 1,850.0 1,850.0 1,950.0 910.2 1,010.2

house Price index Laying the Foundation for Financial Growth

(“HPI”) 1.86% 2.24% 3.60% 3.98% 0.57% 1.55%

consumer Price index

(“CPI”) 2.0% 2.3% 1.6% 1.9% 2.5% 2.8%

Unemployment rate 3.5 3.3 3.2 2.9 4.3 3.7

Gross domestic Production |

additional information & disclosure Summary

(“GDP”) 6.20% 5.30% 6.63% 5.73% 4.20% 3.30%

an increase in unemployment rate or cPi will generally correlate with higher allowances for credit losses, whereas

an increase in the other macroeconomic factors (Klci, hPi and GdP) will generally correlate with lower allowances

for credit losses. due to the unprecedented nature of the pandemic, and the difficulty of predicting reliably the

forecast period, the bank has applied certain management overlay on the overall allowance for credit losses.

|

24 th aGm information